Why Your Home's Value and Your Home Equity Are Not the Same Thing

One of the most common misconceptions I hear from homeowners is:

"My home is worth $500,000, so I have $500,000 in equity."

Unfortunately, that's not how it works.

While your home's value and your home's equity are related, they are not the same thing.

Understanding the difference is important because equity can impact everything from refinancing opportunities and home improvements to retirement planning and future real estate decisions.

Let's break it down.

What Is Your Home's Value?

Your home's value is simply what your property is worth in today's market.

This value is typically determined by factors such as:

Comparable sales

Location

Property condition

Market demand

Inventory levels

Interest rates

For example, if recent comparable homes in your neighborhood have sold for around $500,000, your home's market value may be approximately $500,000.

Think of market value as the price someone may be willing to pay for your home today.

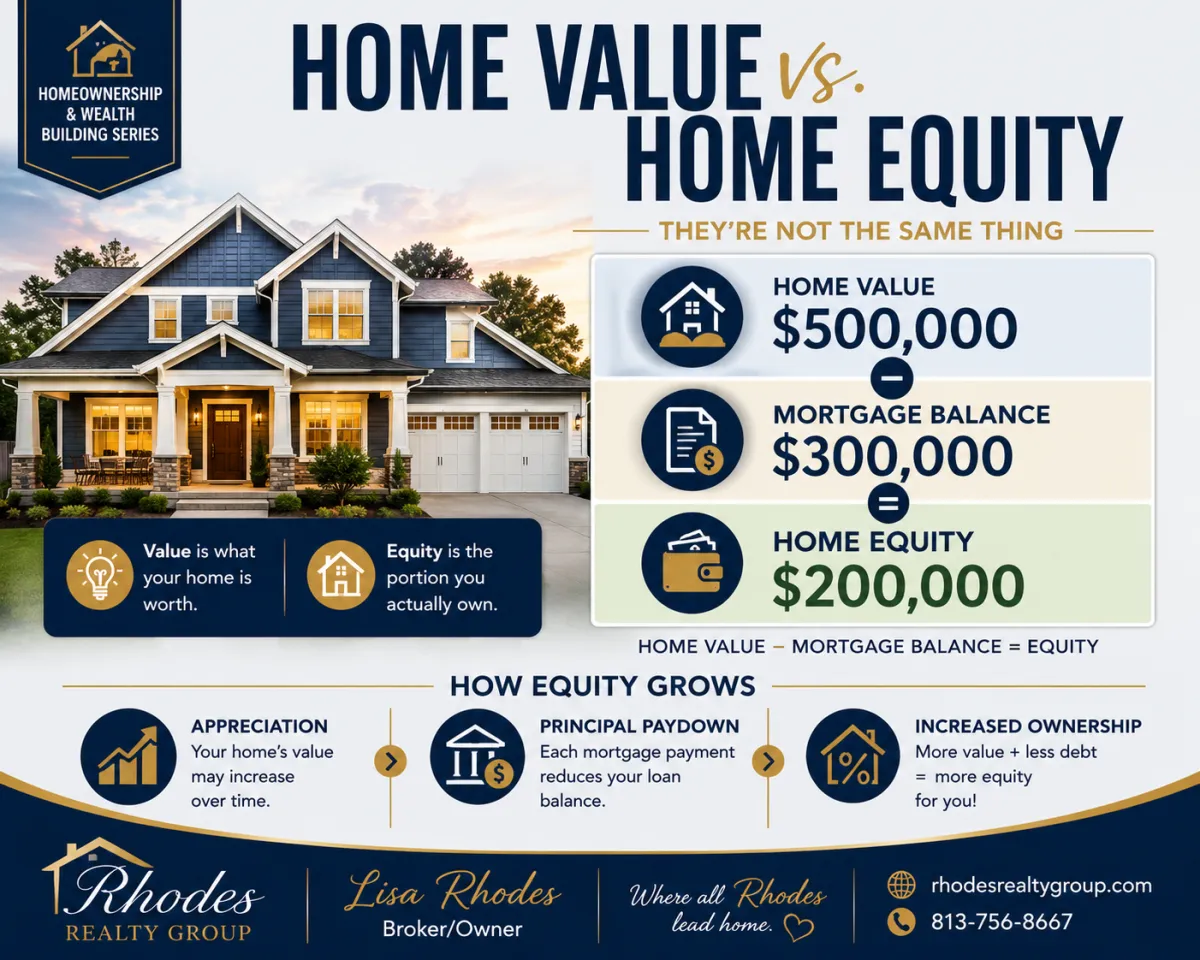

What Is Home Equity?

Home equity is the portion of your home that you actually own.

The formula is simple:

Home Value – Mortgage Balance = Equity

Let's look at an example:

Home Value: $500,000

Mortgage Balance: $300,000

Estimated Equity: $200,000

In this example, the homeowner has approximately $200,000 in equity—not $500,000.

The mortgage lender still has a financial interest in the remaining balance.

How Equity Grows Over Time

There are two primary ways homeowners build equity.

1. Appreciation

When property values increase, equity often increases as well.

Using the previous example:

If the home increases in value from $500,000 to $550,000, the homeowner may gain an additional $50,000 in equity, assuming the mortgage balance remains the same.

2. Principal Reduction

Every mortgage payment helps reduce the loan balance.

As the balance decreases, the homeowner's ownership stake increases.

Many homeowners build equity every month without realizing it.

Why Equity Matters

Equity isn't just a number on paper.

It can create opportunities.

Depending on individual circumstances, homeowners may use equity to:

Move up to a larger home

Downsize and reduce expenses

Fund renovations

Purchase investment property

Support retirement planning

Create financial flexibility

The more equity a homeowner has, the more options they may have available.

Market Value Can Change

One reason it's important to understand the difference between value and equity is that market value is not guaranteed.

Real estate markets move.

Values can increase.

Values can stabilize.

Values can decline.

Equity is influenced by both your home's value and your remaining loan balance.

That's why homeowners should periodically review both.

Why Online Estimates Don't Tell the Whole Story

Many homeowners rely on online home value estimates.

While these tools can provide a general starting point, they often don't account for:

Recent upgrades

Property condition

Unique features

Neighborhood trends

Off-market activity

An online estimate may suggest a value, but it doesn't automatically tell you how much equity you have.

You still need to account for your mortgage balance and selling costs.

Don't Forget Selling Costs

Another factor many homeowners overlook is transaction costs.

If you decide to sell your home, expenses may include:

Closing costs

Title fees

Taxes

Repairs

Moving expenses

Realtor compensation

Those costs can impact the amount of equity ultimately received from a sale.

Why Homeowners Should Monitor Their Equity

Many people track:

Retirement accounts

Investment accounts

Savings accounts

But they rarely monitor one of their largest assets: their home.

Understanding your equity position can help you make informed decisions about your financial future.

It can also help identify opportunities you may not realize exist.

Final Thoughts

Your home's value and your home's equity are closely connected, but they are not the same thing.

Value tells you what your home may be worth.

Equity tells you how much of that value belongs to you.

The difference matters.

Whether you're considering selling, refinancing, investing, downsizing, or simply planning for the future, understanding your equity position can help you make smarter financial decisions.

If you're curious about your home's current market value or would like to better understand your equity position, I'd be happy to help.

I'm Lisa Rhodes, Broker/Owner of Rhodes Realty Group, where all Rhodes lead home.